Numbers don’t lie, but only if the right person is handling them. When it comes to managing your small business finances, hiring a CPA, bookkeeper, or accountant isn’t just a box to check. It’s a strategic decision that can define your company’s growth trajectory.

Most small business owners juggle invoices, receipts, and tax filings while trying to keep the lights on, often confusing the roles of bookkeepers, accountants, and CPAs.

It’s easy to mix them up because all three deal with money, but their expertise, authority, and impact differ significantly. So, here you’ll learn the six key differences between CPAs, accountants, and bookkeepers.

Also, how each role can elevate your small business from simply surviving to financially thriving.

Why This Comparison Matters for Small Business Owners

Running a small business means wearing many hats, like marketing, operations, HR, and finance. Yet, the financial side often determines whether your business grows steadily or struggles silently.

According to a Small Business Administration report, over 82% of business failures are due to poor cash flow management.

That’s where these three financial pros step in. Each has a unique role:

- A bookkeeper keeps your financial heartbeat steady.

- An accountant interprets what that heartbeat means.

- A CPA ensures your business stays healthy, compliant, and tax-efficient.

1. Education, Certification, and Credentials

Bookkeeper

Bookkeepers are your financial record-keepers, they ensure every transaction is recorded accurately. While formal education isn’t mandatory, many complete certifications such as QuickBooks ProAdvisor or Certified Bookkeeper (CB) through the American Institute of Professional Bookkeepers (AIPB).

They may not offer tax or audit advice, but they’re the first line of defence against disorganization and financial chaos.

Accountant

Accountants usually hold a bachelor’s degree in accounting or finance and are trained in principles like GAAP (Generally Accepted Accounting Principles). They can analyze data, prepare financial statements, and help you understand profitability and efficiency.

They bridge the gap between bookkeeping and strategic planning.

CPA (Certified Public Accountant)

CPAs go a step further. They pass the rigorous Uniform CPA Exam, complete 150 college credits, and gain state licensure to practice. Unlike bookkeepers or regular accountants, they can represent clients before the IRS, perform audits, and sign off on official financial statements.

In short, Bookkeepers record. Accountants interpret. CPAs certify and strategize.

2. Scope of Services

Bookkeepers

Their work focuses on day-to-day accuracy, tracking sales, expenses, payroll, invoices, and reconciliations. For example:

- Categorizing transactions in QuickBooks Online or Xero

- Reconciling monthly bank statements

- Generating basic profit & loss reports

This ensures your books are “audit-ready” anytime. A small business that maintains updated books can reduce year-end accounting costs by up to 40%.

Accountants

Accountants turn that data into actionable insight. They create:

- Monthly and quarterly financial reports

- Cash flow forecasts

- Tax-ready statements

- Budgets and KPI dashboards

They help owners see whether that new marketing campaign actually drove profit or whether rising COGS is eroding margins.

CPAs

CPAs handle advanced financial activities:

- Tax planning & filing for businesses and individuals

- Audit and assurance services

- Strategic advisory for business expansion or mergers

- Forensic accounting for fraud detection

When you’re seeking investors, financing, or preparing for an audit, a CPA’s signature carries legal and financial weight.

3. Compliance and Legal Authority

Here’s where things get serious.

- Bookkeepers cannot legally represent you before tax authorities.

- Accountants can prepare returns but not necessarily defend them.

- CPAs are legally authorized to represent you before the IRS and certify audited statements.

For small businesses, this can be crucial during tax season or audits. The AICPA (American Institute of CPAs) reports that over 70% of small businesses face compliance errors that could have been avoided with proper CPA oversight.

So, while bookkeepers keep your records spotless, CPAs keep your business compliant and legally protected.

4. Strategic Impact on Business Growth

Think of financial professionals as levels of strategy:

- The bookkeeper ensures the foundation is solid.

- The accountant builds the framework for insight.

- The CPA adds the upper floors, tax strategy, forecasting, and scalability.

Example:

A small e-commerce business may start with a bookkeeper to track daily sales, then engage an accountant to analyze profit margins, and finally hire a CPA to create a tax strategy that reduces liability by 20%.

Each role builds upon the other, like rungs on a financial ladder.

5. Cost, Value, and ROI

- Bookkeeper: $30–$60/hour

- Accountant: $60–$120/hour

- CPA: $150–$400/hour or project-based

While CPAs come at a premium, they often save you more than they cost by optimizing tax deductions, catching compliance errors early, and advising on profit strategies.

Example:

A CPA can help a small business owner structure as an S-Corp instead of an LLC, potentially saving thousands in self-employment taxes each year.

Pro Tip:

View financial help as an investment, not an expense. A skilled financial team saves you time, ensures compliance, and supports long-term profitability.

6. Technology and Tools

The digital transformation of finance has blurred traditional boundaries.

- Bookkeepers use tools like QuickBooks Online, FreshBooks, and Wave to automate transactions and generate reports.

- Accountants integrate software like Excel Power Query, Xero Analytics, and Fathom for deeper insights.

- CPAs utilize advanced platforms such as Thomson Reuters UltraTax, CCH Axcess, and AuditBoard for tax strategy and auditing.

The right tech stack can reduce manual entry by 80% and give business owners real-time clarity.

Similarities Among CPAs, Accountants, and Bookkeepers

While their roles differ, these professionals share several similarities that make them indispensable to any business:

- Financial Accuracy: All three ensure your numbers reflect reality.

- Data Confidentiality: Each must uphold ethical standards and handle sensitive financial data with care.

- Business Support: Whether tracking daily sales or preparing a tax plan, they all help improve financial health.

- Software Proficiency: They rely on similar accounting systems to ensure consistency and accuracy.

- Goal Alignment: Their shared mission is simple, to keep your business profitable, compliant, and scalable.

Impact on Small Businesses

For small business owners, having the right financial partner is a game-changer.

- A bookkeeper helps you stay organized and makes tax season painless.

- An accountant interprets your financial data and advises on smarter spending.

- A CPA ensures your business is protected, compliant, and structured for maximum savings.

When combined, they offer a full-circle financial solution that strengthens cash flow, reduces errors, and frees you to focus on what matters: “growth.”

By outsourcing to professionals, owners can reclaim those hours and focus on scaling operations.

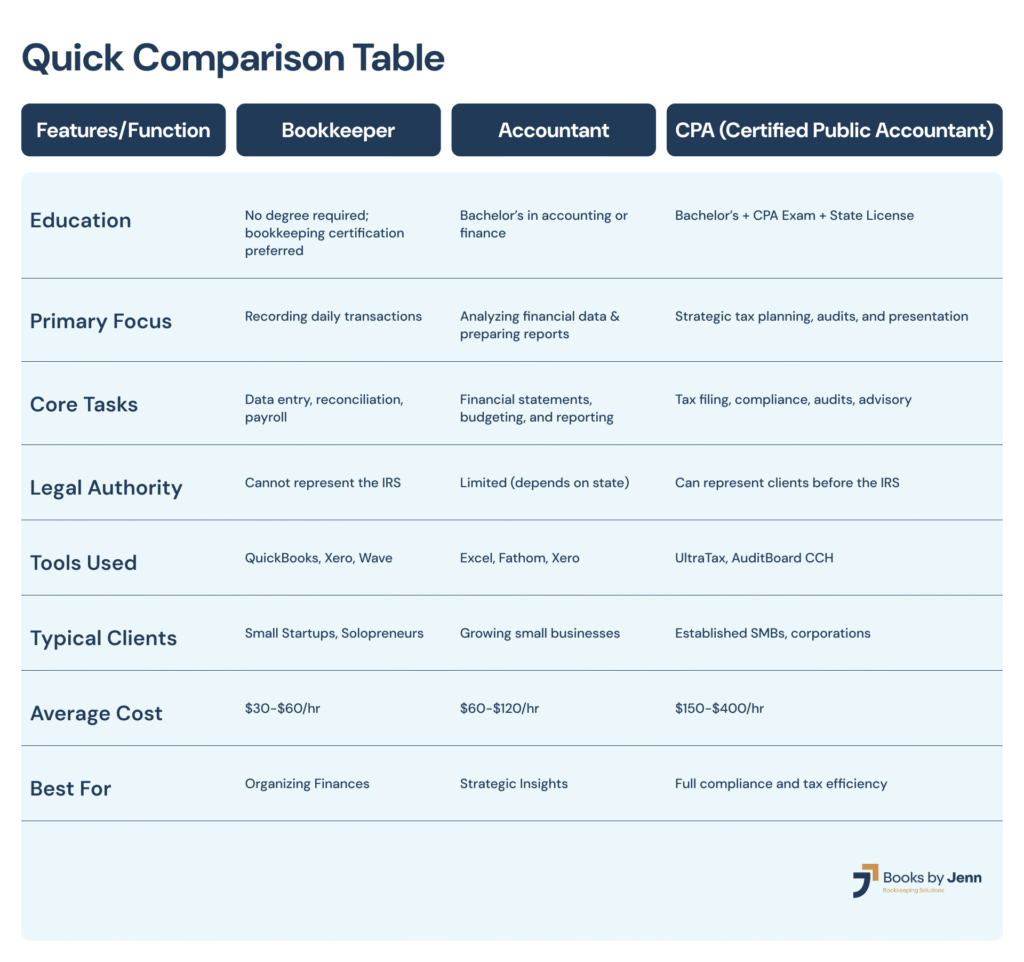

Quick Comparison Table

Final Thoughts: Choosing the Right Fit for Your Business

Each professional serves a different purpose, but together, they build the backbone of your business’s financial success.

If you’re a small business owner:

- Start with a bookkeeper to ensure clean, consistent data.

- Add an accountant as you grow and need analysis and forecasting.

- Engage a CPA for taxes, compliance, and strategic planning.

Like gears in a well-oiled machine, they work best when aligned.

“Behind every thriving small business is a strong financial partnership.”

Want clarity, confidence, and compliance?

Contact Books by Jenn today for personalized bookkeeping and CPA-backed advisory services that help your business grow, without the guesswork.